In Part II of this series we discussed the technical aspects of acquisitions. Part III examines developing the pro form during an acquisition or property sale. Just to keep the record straight, my firm is not a brokerage or real estate advisor, but a very smart engineering company. While we might understand the concept of absorption rates, it doesn’t mean we perform complex real estate analyses. Similarly, just because a real estate broker knows what a UPS system is, doesn’t mean he can design one. However, it is the combined knowledge of the broker and engineer that creates the most accurate and convincing pro forma for both the seller and the buyer.

THE REAL ESTATE ADVISOR MEETS THE CLOUD

In Part IV of “Year-Long Road Trip: Getting to the Total Cost of Ownership (TCO)” (Mission Critical, August/September 2013 issue), I discussed the industry’s most recognized brokerage firms and their leading brokers with in-depth knowledge of the data center industry. The list really hasn’t changed much over the last year. What has changed are the markets that are expanding and the impact cloud providers have in a competitive environment against many colocation and managed service providers. Brokers that do comparison models now have to include cloud offerings in comparison to colocation/managed service providers (MSP). Whereas the typical MSP would provide reboots, cross connects, and other physical services, some have migrated to offer cloud services installing software and utilizing virtualization. When adding cloud software and support, the TCO study and the pro forma are skewed due to the software cost and cloud support during the standard real estate comparison model.

Over the years, the real estate advisor’s role has been expanded to meet the market demand. Ten years ago a broker would have balked at the mention of integrating rent with cost per KW. This, coupled by multiple service offerings by the colocation or wholesale providers, makes it more difficult to get an apples-to-apples comparison.

THE TRADITIONAL MODEL FOR DATA CENTER TCO AND PRO FORMA

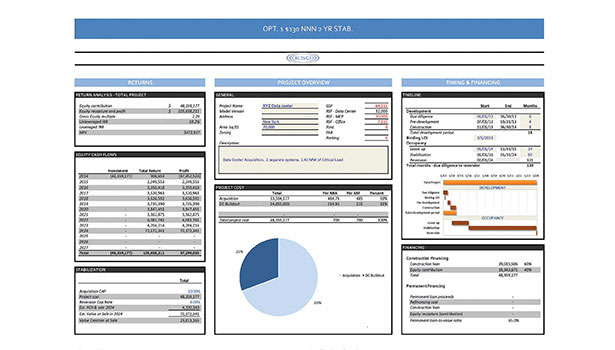

In my last column I discussed the importance of CAPX and OPEX during the acquisition phase. This information combined with the broker’s absorption rates, real estate financial input, and internal rate of return (IRR) has become the basic formula for a successful pro forma. From an OPEX standpoint, the traditional facility infrastructure support cost is always a baseline financial component of the overall pro forma. However, now that we incorporate managed services and cloud offerings, the OPEX concerning people rises dramatically. This OPEX cost, in a comparative model to wholesale, skews the overall price point and ROI of the investment.

From the enduser’s perspective, developing a TCO on build vs. cloud/colo now incorporates cloud services and the reduction of IT personnel. These costs are above and beyond the typical managed services agreements that may be offered within a colocation contract. Therefore, either an enterprise user needs to address all aspects of personnel, real estate, and colocation cost into the TCO or focus on cloud/colo vs. cloud/colo for competitive comparisons. As with most of the larger endusers, typically the recipe is more of a hybrid cloud which outsources a portion of IT offerings such as email. This model too needs to be adjusted within the TCO and pro forma.

FUTURE TCO AND PRO FORMA MODELS NEED TO ACCOUNT FOR RENEWABLE ENERGY

We have discussed traditional pro forma models as well as cloud/colo pro forma models. Moving forward, the industry needs to better address renewable energy from CAPX and OPEX standpoints and integrate the cost and benefits into the overall pro forma. Last month, Greenpeace published its clean energy matrix for public cloud providers, as they have done now for the last couple of years. Public cloud providers such as Apple, Microsoft, Yahoo, and others have increased the usage of clean energy solutions dramatically. However, the wholesale and colocation market has not adjusted its designs to incorporate renewable energy due to cost and trying to stay competitive with the market price. This year, Greenpeace published the same clean energy matrix, and the wholesale and colocation providers scored very low in carbon emissions.

When creating pro forma models and TCO concerning renewable energy, we often find the initial CAPX is increased. However, within every TCO we identify the payback period of each CAPX item and often find that the energy savings justifies the initial investment. In most pro forma models that include renewable energy, the electrical utility charge back is significant, especially in scenarios concerning methane energy sources.

M&A WITHIN THE COLOCATION AND WHOLESALE INDUSTRY

Finally, there has been lots of speculation concerning mergers and acquisitions within the colocation and wholesale data center industry. Over the last five years, the build out of new data centers across the nation has cost REITs a considerable amount of investment, with diminished returns. CAPX expenditures have the biggest impact on ROI and the ability to be competitive.

Currently, the top 15 REIT’s within the industry are struggling to post profits like they did a few years back. What is the most common approach to new growth within other industries? Well, we’ll just have to find out.

Just for the record, I’m not a real estate advisor or broker … I’m an engineer.